MOOOOH

Summary

Molina Healthcare has a good chance of becoming a steadily growing company that I wouldn't fault an investor for holding.

The company has been improving its business results since its new CEO Joseph Zubretsky took.

MOH’s stock is traded at a undervalue in the conservative scenario, according to my DCF model.

The MCC's acquisition will have a positive impact on future revenue.

Founded in 1980 and headquartered in Long Beach, CA, Molina Healthcare Inc. is a multi-state managed care organization participating exclusively in government-sponsored healthcare programs such as the Medicaid program and the State Children's Health Insurance Program (SCHIP), catering to low-income persons.

The company is known for its rapid growth from 2012 to 2017, with a total of 27.4% CAGR (2012-17). There were aggressive bidding wins of Medicaid contracts, as well as an untimely expansion into the health insurance market (via the Affordable Care Act). It was a shaky story accompanied by the reckless decisions which was well described in an article published a few years ago.

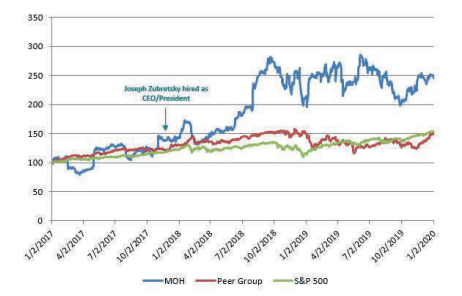

In 2017, MOH went through a crisis, but with the resignation of J. MOH. Mario Molina and John Molina and the appointment of Joseph Zubretsky as the new CEO, stock and profit growth resumed, as you can see in the picture below:

Source:Year-End 2019 Molina Healthcare Financial Report

It is important to add that the share growth is ahead of other competitors, and grows in a falling market. The price has recently broken out the main resistance at $160 per share. Before that, share price approached this resistance level on the news that Sanders suspends campaign.

The financial report for the first quarter of 2020 has been released. Premium revenue for the first quarter increased 8.9 percent year on year to $4.3 billion, while its total revenue is $4.5 billion, up from $4.1 billion in revenue it reported for the first quarter of 2019. Mostly due to the Medicaid and Medicare divisions.

However, if we look at the annual revenue figures for several years, it becomes clear that overall the company's revenue is decreasing and constitutes 1.71% CAGR for the last 3 years. This is mainly because the company is leaving unprofitable divisions and overall it is a good sign of the ongoing restructuring.

Under the leadership of the new CEO, the company has been steadily reducing its operating expenses starting from 2017. For instance, 13.2% and 11% in 2018 and 2019, respectively. Although, total operating expenses increased 11.4% year over year to $4.2 billion due to higher medical care costs, depreciation, and amortization. As a part of this initiative, the company sold its units, Pathways Health and Community Support, LLC, and Molina Medicaid Solutions, which is expected to help it focus on core growth areas.

Also, the company has mixed results in Texas. The Molina unit in Texas reports that the Human Services Commission (HHSC) has notified that it will terminate all STAR+PLUS re-procurement contracts, including the solicitation from Molina Healthcare of Texas. The HHSC is currently "deliberating" the next steps in the matter.

Some sell-side analysts consider HHSC's decision to be a net positive for Molina, as there may be a significant delay in issuing a request for new proposals due to the disruption of COVID-19.

Cost of goods sold or MCR in the first quarter of 2020 increased to 86.3% compared to the first quarter of 2019, which amounted to 85.3%. Let's see what caused the increase in this indicator in the picture below.

Source: Molina Healthcare Reports First Quarter 2020 Financial Results

As we can see, Medicaid was stable. And in contrast, in the Medicare business, the MCR for the first quarter of 2020 was 81.7% compared to 84.7%, in the first quarter of 2019, due to rate increase and higher quality incentive revenues. And the decline of the MCR by almost 20 points in Marketplace was due to the company's price reduction to be more competitive.

The G&A ratio for the first quarter of 2020 increased to 7% compared to 7.3% in the first quarter of 2019, primarily due to revenue growth and positive operating leverage. The company's quarterly M&A ratio reflects approximately $6 million of additional costs associated with the mobilization of our home-based employees, along with other COVID-19-related operating protocols.

COVID-19 impacts

The recession and unimaginable reduction in U.S. hiring will have a positive impact on the company's key operating performance. According to Dean Ungar, the vice president of Moody's Investors Service:

Molina Healthcare, Inc’s earnings in Q1 2020, were not materially impacted by the coronavirus. Its EBITDA margin of 6.6% compares favorably with its government-focused peers.We believe the company is well-positioned to manage the coronavirus, even if its severity and duration are worse than suggested by current trends. As a Medicaid-focused company, membership growth is likely to be driven by the economic downturn.

U.S. hospitals are losing about $50B per month due to a large number of cancellations of elective treatments, costs associated with treating COVID-19, and an increase in the number of uninsured patients. CEO of the American Hospital Association, Rick Pollack said:

I think it's fair to say that hospitals are facing perhaps the greatest challenge that they have ever faced in their history, calling the situation a "triple whammy".

However, the net impact on U.S. health insurance companies will be the exact opposite and will be positive for them, the costs from COVID-19 will be very small and more than outweighed by the delayed elective procedures.

Also, it is interesting to know how strong the growth of Medicaid members has been already in April.

Thus, according to the company's information, the growth at the end of March and April will be probably more by 30'000 members in Medicaid compared to the same period last year. And what the most important, most likely, is that the members are truly due to the suspension of eligibility in the states. And we will only see changes in the number of Medicaid members in the second quarter of 2020.

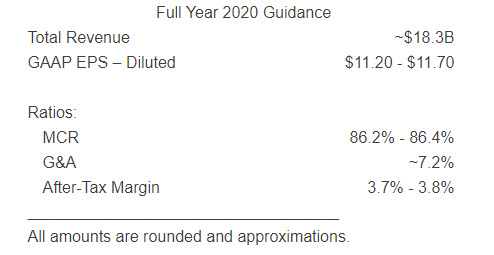

Guidance of 2020

Over the last year of 2019, the company has confidently met its expectations set for 2019. Premium revenue was $16.2 billion. The medical care ratio was 85.8%, as the company's efforts to contain costs continued to control medical expenses while ensuring the highest quality of service to its members. The G&A ratio was 7.7% as they used a fixed cost base and began investing in growth.

According to CEO Molina Healthcare Joe Zubretsky:

We improved our Medicaid and Medicare margins and earned exceptionally high margins in our Marketplace business. The 2019 total company after-tax margin of 4.4% was supported by 3.2% in Medicaid, 6.7% in Medicare, and 10.3% in the Marketplace. All in, this performance resulted in a net income of $737 million and earnings per diluted share of $11.47. In a year when premium revenue decreased by 8% due to legacy contract losses, we were able to deliver 4.4% after-tax margins and earnings per share growth of 8%, a testament to our early-stage focus on margins. During the year, we improved an already-strong balance sheet and capital structure while the business continued to generate significant excess cash flow.

For 2020 guidance, CEO informs:

The two factors that we updated in our guidance are one that's sort of easy to understand and engage. And that is our portfolio is going to roll over into lower-yielding investments. It's irrefutable and already happening. And I think Tom pitched that as a $27 earnings per share $0.27 earnings per share headwind in our guidance. We also believe putting the accelerated membership aside that we will incur higher SG&A related to COVID-19 operational protocols, financial assistance to our employees, etc, which also we factored into our the reaffirmation of our guidance, but we did not update for anything else.

Molina has solid 2020 guidance. MOH reaffirmed its initial guidance despite the COVID-19 effect. Total revenues are expected to be $18.3 billion, suggesting an 8.7% increase from the year-ago reported number. The company anticipates earnings in the range of $11.20-$11.70 per share.

Source: Molina Healthcare Reports First Quarter 2020 Financial Results

Against the background of strong positions on the balance sheet, the company directs capital to increase shareholder value. The company's Board of Directors approved a share buyback plan for up to $500 million. Cash flow from operating activities also improved significantly in 2019 due to the timing of bonuses and government payments. Molina Healthcare completed a $500 million share buy-back program. In the first quarter, the company bought back $450 million worth of shares. The company's impressive capital management position should attract investors' attention. The firm completed a $500 million share buyback program. In the first quarter of 2020, MOH bought back a total of 3.4 million shares for approximately $450 million.

MCC is purchased by Molina Healthcare Inc.

Despite the breakdown of the purchase of Next Level, MOH's top management was not desperate and informed investors about the M&A with Magellan Complete Care (MCC) with a total deal value of $820 million.

The deal is forecasted to be closed in the first quarter of 2021, will serve more than 3.6 million members through publicly funded health programs in 18 states. This is expected to enable the company to build a better service portfolio, expand its geographic reach. The transaction is predicted to increase by about 50 to 75 cents of cash income per share in the first year of ownership and at least $1.75 of cash income per share in the second year of ownership.

This is positive news for the company. It will expand its Medicaid footprint and boost earnings. Also it will allow us to scale enterprise-wide platforms and benefit from both operating and fixed cost leverage.

Pro-forma' projected revenue for 2020 is over $20 billion. Revenue from this transaction is expected to increase by approximately $3 billion by 2021. Molina believes that the acquisition will help achieve it's planned margin.

Let's talk about what kind of company MOH is buying and what awards it will give for the future of the company.

First of all, you need to understand that the acquired company has its own pledged growth rate. According to the press conference, the full-service Medicaid contract is at its very early stages in Arizona from about 13,000 members at the end of the year with a growth forecast to 75-80,000 over the next year. Because it enjoys a preferred position in the auto-assignment algorithm in the state.

Accordingly, with the geographic expansion of its presence in the new states, the company will launch a DSNP product in its marketplace product there. By purchasing one unit, MOH adds to the companies portfolio three new states and three states with expired terms of validity at a purchase price of approximately 30% of the target revenue.

As of 31 December 2019, MCC served approximately 155,000 members in six states, Virginia, Arizona, Massachusetts, New York, Florida, and Wisconsin. Revenue for the full year 2019 was over $2.7 billion and MOH forecast it to grow to $3 billion within two years. And, of course, just being in New York City's Westchester neighborhoods gives them plenty of opportunities to find additional opportunities in the city and perhaps to grow their business.

Management said during the Q1 conference call:

And if you can then pack on positive operating leverage, because we're not going to increase the fixed cost base of running our enterprise when we take these on, you can easily see how we got to the $0.50 to $0.75 of accretion in the first full year of ownership and at least $1.75 of cash earnings per share accretion in the second full year of ownership. So in the first year of ownership, we will most likely operate on their cost structure as integration activities take place. In year two, we will be migrating to the Molina cost structure, both our G&A platforms and the impact of payment integrity, utilization, management, and risk or quality will begin to improve the medical cost ratios. And sometime in year three, we should reach the margins that we enjoy today in the moving of portfolio.

The $820 million transactions, net of certain tax benefits, is expected to close in the first quarter of 2021.

DCF analysis

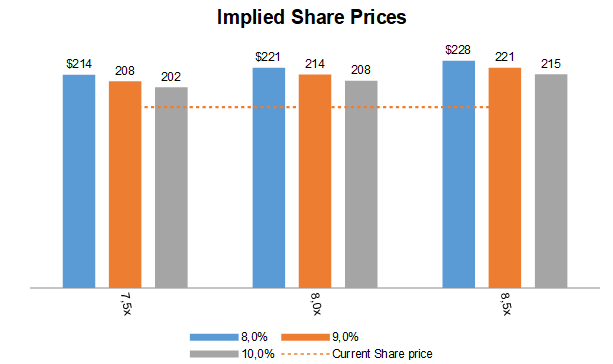

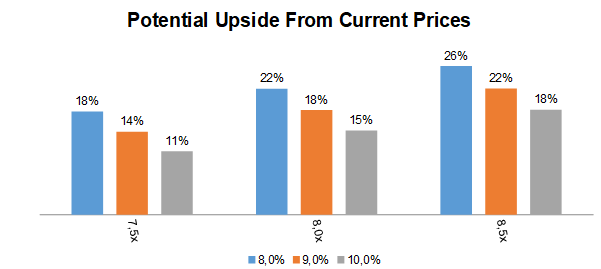

DCF, a metric widely used to find undervalued shares, it will help us understand whether the company has a fundamental upside. In my DCF model, in the baseline scenario, I calculated with these assumptions:

- Revenue growth of 7.8% by the end of 2020

- Added 3'000 mil. of revenue by 2021, which is likely to come from the acquired company

- CAGR 2021-2024 I put the moderately, according to analysts' forecasts, at 4.4%.

- The personal required rate of return - 10%

My model shows that after subtracting the total debt, add cash and investments, and other issues then the market value of equity is around $9'000 million in the base scenario.

After all the calculations, it turns out that the true share price including DCF metrics is $214, which is 18% higher than the current share price ($181.54 as of writing).

The range of true stock prices according to my model is from $202 to $228, which is 11% to 26% respectively.

Simply Wall St. Fair Value according to their 2 Stage Free Cash Flow to Equity is even $434, which is 202% higher than my forecast. The share price is 57% below the Fair value.

Source: Author's DCF model

Source: Author's DCF model

Source: Simplywall.st

Conclusion

In summing up, I will note the strengths and weaknesses of the company.

First of all, their strong management. Competent management of the company's finances, victory in the competition for new contracts for the provision of medical services to Medicare and Medicaid, as well as the distribution of net profit for the share buyback in 2019-2020.

Second, financial stability. The availability of adequate financing on acceptable terms to fund and capitalize expansion and growth, repay outstanding indebtedness at maturity, and meet general liquidity needs. And, it should be noted that the cash and cash equivalent is $2375 million. It is also the ability to transfer part of the company's profits to its shareholders, as well as the ability to buy smaller companies to reduce the COGS (MCR) and general and administrative costs (SG&A) and increase its influence in other U.S. states where it is not yet represented, which will also increase the company's revenue.

The large M&A transaction opens up opportunities to reduce costs for both companies, as well as revenue growth due to the penetration of other products into new markets.

Eventually, combination of all these factors creates a great fundament for future revenues and growth of shares.