Further Evidence of Bitcoin Price Manipulation.

CryptoClub: this article, an excerpt of research on #BTC manipulation

Executive Summary.

- Unmolested prices have been shown to exhibit an

expected, natural distribution characterized by

Benford’s law. Benford’s law has been used to

identify and investigate financial anomalies and

fraud for nearly 30 years. We believe this is the

first application of Benford’s law to bitcoin. - We can say with nearly 100% confidence that

bitcoin’s price was manipulated at some point

since 2010. We can say with 95% confidence that

bitcoin’s price was manipulated in 2013, 2017,

and 2019. Our research corroborates the general

findings of Gandal [2018] and Griffin [2020].

Bitcoin’s price during these periods is not reflective

of natural supply and demand by equally

motivated buyers and sellers. - Both technical and fundamental analysis of bitcoin

that include suspect periods is likewise suspect

unless the issue is recognized and adjustments are

made. When price has been manipulated, any

comparisons of price to fundamental metrics

would be flawed. Such analysis is likely to have a

detrimental impact on both the assessment of

current value and forecasts of future price.

Prior Research.

Past research on this topic includes Monamo [2016],

Gandal [2018] (which is contemporaneously

summarized at reference note 18), Chen [2019],

Bitwise [2019], and Griffin [2020].

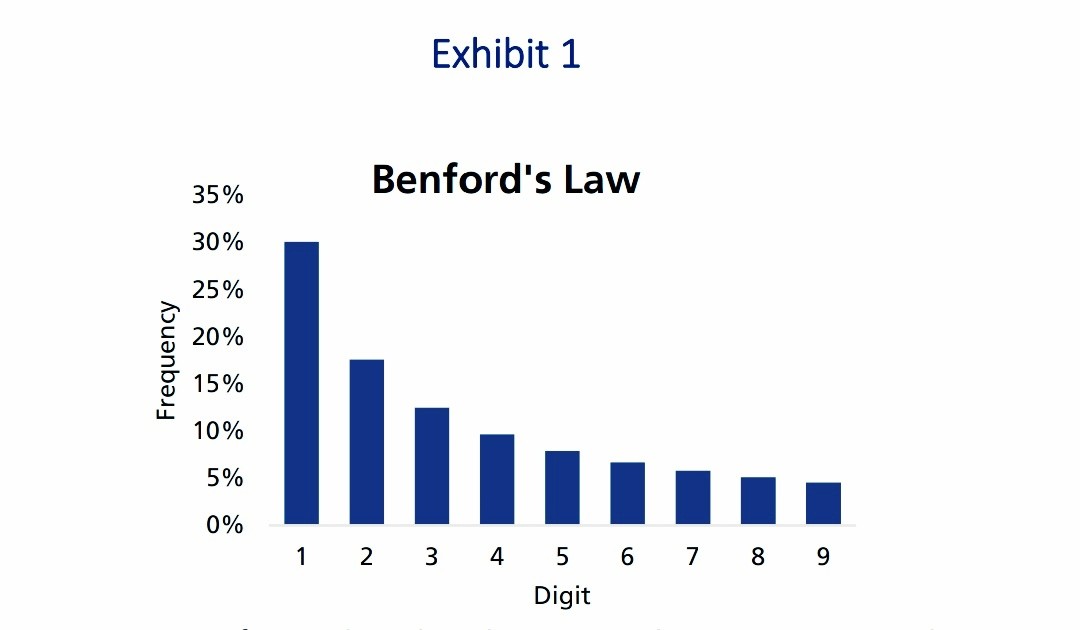

Benford’s Law.

Benford's law is an observation about the frequency

distribution of leading digits in many real-life sets of

numerical data. The law states that in many naturally

occurring collections of numbers, the leading

significant digit is likely to be small [Benford, 1938].

Specifically, the number 1 appears as the leading

significant digit about 30% of the time, while 9

appears as the leading significant digit less than 5%

of the time. Benford's law also makes predictions

about the distribution of second digits, third digits,

digit combinations, and so on. A Benford distribution

resembles a Pareto distribution

(Exhibit 1).

Deviations from this distribution indicate an anomaly,

and typically that anomaly is caused by some type of

fraud. Application of Benford’s law to fraud detection

dates to at least Varian [1972] as a test of validity of

scientific data. It has been used to assess reported

earnings [Carslaw 1988], [Thomas 1989], tax

compliance [Nigrini 1996], and auditing [Durtschi 2004].

Data and Methodology.

Data is sourced from the daily price history dataset

from coinmetrics.io.

We use the methodologies set out in Benford [1938],

Durtschi [2004], and Stambaugh [2012]. We use the

first-, second-, and third-digit tests. For bitcoin prices

less than $1.00 we ignore leading zeros after the

decimal.

To ensure there is statistical significance in our

distribution results, we required that each bin [0..9] in

our histogram be populated with at least eight

observations. If this condition is not met for the first-digit test, we rely on the second-digit test. If this

condition is not met for the second-digit test, we rely

on the third-digit test.

A key reason for this approach is that there could be

extended periods where the first digit may only be

comprised of one or two unique numbers. For

example, the S&P 500 started with a “1” or a “2”

from 2009 to 2019. First-digit Benford analysis over

this time period would be meaningless.

We conducted an analysis for the entire period July

2010 through June 2020. We also conducted analyses

for calendar years 2011-2019 (we exclude the 2010

and 2020 partial years as having too few

observations.) Because Benford analysis requires large

datasets, it is difficult to narrow down anomalies to a

granularity of less than one year.

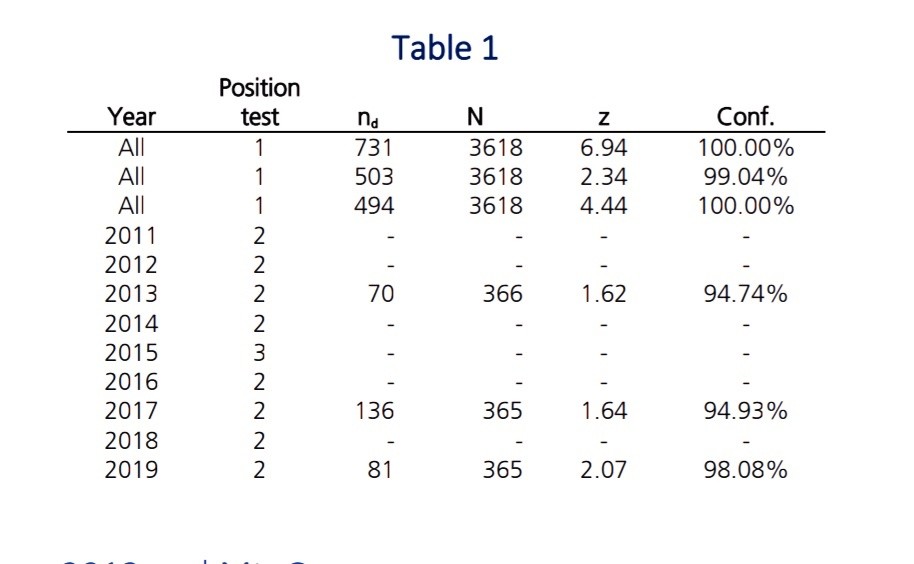

Empirical Results.

Table 1 shows results for those tests where there was

a 90% or greater probability of anomalous pricing.

Position test indicates whether the first-digit, second-

digit, or third-digit test was used.

nd is the number of observations in the bin where an

anomalous result was detected. This is not the

number of anomalous events. nd / N gives the

observed distribution, whereas the expected

distribution is governed by Benford’s law.

N is the total number of observations in the test.

z is the z-score for the test.

Conf. is the assumed normal distribution confidence

level that an anomalous event occurred during the

tested period.

nd / N nd / N gives the observed distribution, whereas

the expected distribution is governed by Benford’s

law.

1* See Gandal, 2018. “Price Manipulation in the Bitcoin

Ecosystem.”

https://www.youtube.com/watch?v=N0033FbywEg

Discussion.

To those familiar with prior research on bitcoin price

manipulation these results are not entirely surprising.

What is unique is that a commonly accepted and

independent methodology corroborates evidence of

price manipulation.

2013 and Mt. Gox

Gandal [2018] relates that the 2013 manipulation

started with a hack and stolen bitcoins, followed by a

software program (aka “bot”) that engaged in

“painting the tape.” Painting the tape involves

publishing false volume and trading figures to induce

investors to trade. A report by Bitwise [2019]

indicated that this practice is widespread even

recently.

At trial, the CEO of Mt. Gox admitted such bots were

running on the exchange in 2013, cementing the

notion that price was being manipulated.1

Peterson

[2018] confirmed Gandal’s findings using price

deviation from fundamental value.

2017 and Bitfinex.

Griffin [2020] implied that price was manipulated in

2017. One way to manipulate bitcoin’s price is to

issue a relatively worthless new token, and use that

token, say Token X, to purchase bitcoin. The problem is that it will take many X tokens to buy enough bitcoin

to impact price. Issuing more Token X only devalues

Token X further, making it even more difficult to buy

bitcoin. However, if Token X were pegged to a fiat

currency like the dollar, Token X would not lose value

in the short term.

The purported scheme is that investors use dollars to

buy stablecoin Token X, meaning Token X is “backed”

by dollars. Token X is then used to buy bitcoin.

If Exchange X and Token X are affiliated, then

Exchange X can issue IOUs to purchase Token X.

Token X is then used on Exchange X to bid up the price

of bitcoin. Bitcoin is later sold at an inflated price for

dollars, which is deposited into Token X’s account to

retire the IOU, giving the appearance, ex post facto,

that Token X was backed by dollars all along.

Anonymous blogger Bitfinex’d [2017] alleged this was

the scheme perpetrated by Tether and Bitfinex, in

response to a hack and theft of bitcoins on the Bitfinex

exchange in 2016. The allegation was apparently

enough that the U.S. Department of Justice opened

an investigation into the matter [Robinson 2018].

Subpoenas were issued [Leising 2018], but the status

of that investigation is to date unknown.

Benford analysis is unable to ascertain the cause of

fraud or price manipulation, let alone identify

perpetrators. Technically, it only provides evidence of

a deviation from an expected distribution. Our

analysis of 2017 prices cannot confirm specific

allegations of fraud, it can only confirm that the price

behavior of bitcoin in 2017 was unnatural, with

fraudulent manipulation being the most likely

explanation.

2019 and PlusToken.

We are unaware of any studies (published or

otherwise) providing evidence of fraud or price

manipulation in 2019. There are allegations that a

ponzi scheme known as PlusToken may be

responsible. PlusToken was a classic ponzi scheme

that lured unsuspecting victims to invest with promises

of high returns and low investments [Michael 2020].

From January 1 – June 30, 2019, bitcoin gained 212%

to nearly $13,000. Shortly thereafter, bitcoin’s price

declined until December of that year where it traded

around $7,000. Operators of the scheme left a note

“Sorry we have run” in June 2019 and were arrested

by Chinese authorities on June 29th. This period (and

into July) corresponds with bitcoin’s price peak for

2019.

Presumably, the scheme involves

a) selling a worthless token PlusToken to

naïve investors for fiat currency;

b) purchasing bitcoin with PlusToken and

bidding up the price; then

c) selling bitcoin at an inflated price for

fiat currency.

If that is in fact the scheme, then this appears to be a

poor attempt at money laundering as well as price

manipulation.

Our research method cannot validate any such

specifics, only that prices in 2019 are suspected of

being manipulated. The PlusToken scheme, however,

appears to be more than a coincidence.

Conclusion.

Unmolested prices have been shown to exhibit an

expected, natural distribution characterized by

Benford’s law. Benford’s law has been used to identify

and investigate financial anomalies and fraud for

nearly 30 years. We believe this is the first application

of Benford’s law to bitcoin.

Our analysis confirmed anomalies in bitcoin prices for

2013, 2017, and 2019. Given past research on the

topic, we can say with near 100% confidence that

bitcoin’s price has been fraudulently manipulated at

some point in its lifespan since 2010. We can say with

95% confidence that bitcoin was manipulated in

2013; 95% confidence that bitcoin was manipulated

in 2018; and 98% confidence that bitcoin was

manipulated in 2019.

The implications for bitcoin valuation are profound.

First and foremost, it means that technical price

analysis of bitcoin over the suspect periods is likely

meaningless; bitcoin’s price did not reflect equally

motivated buyers and sellers, and therefore bitcoin’s

price cannot be indicative of market psychology.

Also, this finding means that even fundamental

analysis of bitcoin is problematic. Fundamental

analysis typically relies on historical relationships

between price and some other metric to ascertain if

an asset is overvalued or undervalued. When price has

been manipulated, any such comparisons are then

skewed, and would likely have a detrimental impact

on both the assessment of current value and forecasts

of future price.

References.

1. Benford, F. 1938. “The Law of Anomalous Numbers.”

Proceedings of the American Philosophical Society. 78(4):

551-572. https://www.jstor.org/stable/984802

2. Bitfinex’d. 2017. “Bitfinex never ‘repaid’ their tokens, Bitfinex

started a ponzi scheme.”

https://medium.com/@bitfinexed/bitfinex-never-repaid-their-

tokens-bitfinex-started-a-ponzi-scheme-86a9291add29

3. Bitwise Asset Management. 2019. “Meeting with Bitwise

Asset Management / Presentation to the U.S. Securities and

Exchange Commission.” https://www.sec.gov/comments/sr-

nysearca-2019-01/srnysearca201901-5164833-183434.pdf

4. Carslaw, C.A.P.N. 1988. “Anomalies in Income Numbers:

Evidence of Goal Oriented Behavior.” The Accounting

Review. 63(2): 321-327.

5. Chen, W., et al. 2019. “Market Manipulation of Bitcoin:

Evidence from Mining the Mt. Gox Transaction Network.”

IEEE INFOCOM 2019 - IEEE Conference on Computer

Communications, doi:10.1109/infocom.2019.8737364.

6. Durtschi, C., et al.2004. “The Effective Use of Benford’s Law

to Assist in Detecting Fraud in Accounting Data.” Journal of

Forensic Accounting. 5: 17-34.

7. Gandal, N., et al. 2018. “Price Manipulation in the Bitcoin

Ecosystem.” Journal of Monetary Economics. (95): 86–96.,

doi:10.1016/j.jmoneco.2017.12.004.

8. Griffin, J. M., and A. Shams. 2020. “Is Bitcoin Really

Untethered?” The Journal of Finance, forthcoming,

doi:10.1111/jofi.12903

9. Leising, M. 2018. “U.S. Regulators Subpoena Crypto

Exchange Bitfinex, Tether.” Bloomberg.

www.bloomberg.com/news/articles/2018-01-30/crypto-

exchange-bitfinex-tether-said-to-get-subpoenaed-by-cftc

10. Michael. 2020. “Plus Token (PLUS) Scam – Anatomy of a

Ponzi.” Boxmining. https://boxmining.com/plus-token-

ponzi.

11. Monamo, Patrick, et al. 2016. “Unsupervised Learning for

Robust Bitcoin Fraud Detection.” Information Security for

South Africa (ISSA). doi:10.1109/issa.2016.7802939.

12. Nigrini, M.J. 1996. “Taxpayer Compliance Application of

Benford’s Law.” Journal of the American Taxation

Association. 18(1):72-92.

13. Peterson, T. 2018. “Metcalfe's Law as a Model for Bitcoin's

Value.” Alternative Investment Analyst Review. 7(2): 9-18.

14. Robinson, M., and T. Shoenberg. 2018. “Bitcoin-Rigging

Criminal Probe Focused on Tie to Tether.” Bloomberg.

https://www.bloomberg.com/news/articles/2018-11-

20/bitcoin-rigging-criminal-probe-is-said-to-focus-on-tie-to-

tether

15. Stambaugh, C., et al. 2012. “Using Benford Analysis to

Detect Fraud.” Internal Auditing. May/June:21-29.

16. Thomas, J.K. 1989. “Unusual Patterns in Reported

Earnings.” The Accounting Review. 64(4): 773-787.

17. Varian, H.R. 1972. “Benford’s Law.” The American

Statistician. 26: 65-66.

18. The Willy Report. 26 May 2014. “Proof of Massive Fraudulent

Trading Activity at Mt. Gox, and How It Has Affected the Price

of Bitcoin.” willyreport.wordpress.com/2014/05/25/the-willy-

report-proof-of-massive-fraudulent-trading-activity-at

Information disclosure.

CryptoClub Digital Research Notes are Research Memorandums that

not peer reviewed and not intended for official

publication in any academic journal.

This document is for informational purposes only. Opinions

expressed in this document are solely those belonging to the Cane Island alternative

Advisors, LLC unless otherwise stated. Material

The data presented have been obtained from reliable sources and not

representations made by us in relation to other parties

informational accuracy or completeness.

The information presented here is not an offer

sell or offer an offer to sell or buy any security in any

jurisdiction. This document does not contain sufficient information

for a potential investor to make an investment decision and any

the information contained in this document should not be used as a basis for this

target.

The content of this document is not

recommendations or take into account a specific investment

goals, financial situation or needs of any future

investor. Investors should not interpret the content of this

document as legal, tax or investment advice and should be consulted

with his digital investment advisor (s)

assets, cryptocurrency or any securities or commodities. last

performance does not necessarily indicate future performance.

The price and value of the assets mentioned in this study, and

income from them can fluctuate. Fluctuations in exchange rates

can negatively affect value, price, or income

received from certain investments.

This document contains information from third parties

sources that have not been verified. As for information

what can be demonstrated cannot be guaranteed as to its accuracy

or suitability for any purpose.

CryptoClub provides its clients with information services, analytics and market trading services (trading recommendations and strategies. Online trading and trust management of the investor's capital. Maintenance of investment capital and its correction.) Registration is not

imply a certain level of skill or training.

© 2020