Gresham’s Law: Bad Money Drives Out Good

In today’s post we talk about AMM pools and Gresham’s law.

Curve is an AMM DEX designed primarily for swapping stablecoins and the most important source of on-chain liquidity (and therefore price discovery) in stablecoins. We alerted on Twitter that the UST-3pool metapool was becoming imbalanced. What does this mean?

Normally a pool will have a fairly equal weight of assets: around 50/50 for an ordinary two asset pool and ~33/33/33 for Curve’s 3pool (USDT, USDC, DAI). This is because liquidity providers begin by depositing an equal amount of each asset.

When trading starts, excess demand for one asset will reduce that asset’s share of the pool but also increase its price slightly. This allows arbitrageurs to profit by supplying the scarce asset at a premium and restoring balance to the pool.

Therefore pools should usually tend towards balance.

Imbalances are typically caused by large swaps. An efficient market will allow individual arbitrageurs to profit by rebalancing the pool and this should happen quickly due to competition.

So why might a pool become increasingly imbalanced over several hours to days?

To answer this, we consult the economic theory named for 16th century English merchant and financier Sir Thomas Gresham.

Until modern times, currency typically circulated in the form of coins made from precious metals. Governments used their monopoly on creating currency as a revenue source, earning ‘seigniorage’ - the difference between the minting cost of a coin and its face value. In times of financial crisis (or desire for additional seigniorage profits), governments debased their currency by issuing coins which contained less precious metal than their face value (by mixing precious and base metals). By law, merchants were forced to accept the debased coins at face value rather than precious metal value.

To further complicate matters, citizens would ‘clip’ or ‘shave’ small pieces off each coin to be melted down for their precious metal weight value. It was therefore difficult to ascertain the precise value of each coin.

In 16th century England, the “Great Debasements” under kings Henry VIII and Edward VI had destroyed confidence in the currency. Sir Thomas wrote to advise the incoming queen, Elizabeth I of England, on restoring financial confidence.

Gresham’s key observation is that ‘bad money’ would drive out ‘good money’ when both were forced (by legal tender laws) to exchange for the same price. This is because buyers of goods would always choose to pay with the debased coin while hoarding the valuable coin. And so the unadulterated coins would leave the market - in fact they were often shipped abroad to be melted down for their precious metal content (where the metal value exceeded the face value of the coin).

Now the link to AMMs becomes clear.

A stableswap AMM pool will force all assets to exchange at the same price until the pool is extremely imbalanced. That is the much lauded capital efficiency of the Curve’s stableswap invariant but this is only useful when the assets indeed have an equivalent *fundamental* value e.g. both USDC and USDT being redeemable for $1.

An AMM is a dumb algorithm which cannot assess the various risks of the privately issued money we call stablecoins. UST is not redeemable for $1 and therefore probably shouldn’t be paired with USDC, which is. The UST-3pool was programmed that 1 UST = 1 DAI = 1 USDT = 1 USDC (all of these are supposed to be worth $1).

When the market suspected that UST may be ‘bad money’, but the algorithm forces it to exchange at the same price as the ‘good money’ tokens USDC / USDT / DAI, the result according to Gresham’s law is that only the ‘bad money’ will remain in the pool.

Bad money drives out good (when both are forced to exchange for the same price).

The UST metapool becoming imbalanced was the first sign that the UST peg may be vulnerable.

Later, the 3pool itself became imbalanced holding ~80% of reserves in USDT.

By understanding the principals behind Gresham’s Law it was possible to come up with a high expectation trade thesis:

BowTiedIguana @BowTiedIguanaEveryone borrow Tether and swap for USDC Thank me later

The exchange rate went 5% off peg a few hours later, making it exteremely profitable to have borrowed Tether and swapped for USDC.

This law applies to other similar assets which are forced to ‘exchange for the same price’ in a stableswap AMM. Take Lido’s Staked ETH (“stETH”) which has now also depegged:

You can monitor the pool here. If this depeg continues, leveraged users are at the most risk. People that have staked their ETH, received stETH then taken that stETH to borrow funds. Some people may have also restaked and added additional leverage. Some discount is of course warranted due to illiquidity and risk that the merge doesn’t happen or is significantly delayed. The thread by Hasu below highlights why a depeg is not some catastrophic event - we generally agree with the thoughts below.

Hasu⚡️🤖 @hasuflIn the last week, the stETH/ETH exchange rate has slightly declined in secondary markets here‘s some thoughts on why they traded at pair to begin with and why the current events are both natural and healthyMay 14th 202272 Retweets385 Likes

Autist note: Close to 30% of ETH is now staked in liquid ETH2 pools. Of the 4.55 million ETH staked, 4.1 million is staked with Lido (91% market share). A hack of Lido Finance (however seemingly low it may be) represents a systemic risk to Ethereum greater than the DAO hack in 2016 which lost 3.6 million in ETH and required an intervention to alter the state of the Ethereum blockchain. One of the debates in the Ethereum community right now is whether or not Lido should put in place a cap to how much ETH can be staked with them to preserve Ethereum’s credible neutrality. As a business, Lido of course does not want to hurt their growth prospects and put themselves in a position to be less competitive down the line. In the long run, it may not matter as more competitors arise but this is an area worth watching.

The meta-point is that it pays very well to know your financial history. There is nothing new under the sun. Sir Thomas Gresham’s letters to the Queen of England were written 464 years ago. John Law’s experiments with the currency of Régence France ended 302 years ago (Olympus DAO). Few people are curious, so by learning from first principles and comparing historical contexts you can find an edge.

Summary: the financial system is not in its final form. A system designed and used by humans will be constantly evolving. History shows us this clearly. Protect your capital - there will be some generational opportunities to come.

Actions

You’re reading us for alpha and actionable information as well as a framework to analyze markets. A few simple bullet points

- monitor Curve pool imbalances as an early alert of market instability

- get off stables - USDT and USDC are centralized, DAI is centralized by the back door (backed by USDC)

- get out of any centralized custody except for amounts you can afford to lose (if you’re a trader you can take on leverage to reduce your counterparty risk but need to manage your margin closely - basic treasury management)

- get out of yield farming, it’s negative expectation at this stage in the cycle

- if you don’t want any crypto directional exposure, rather than going into stables consider selling OTC (check tax consequences) or hedging:

- hedging: you can own spot ETH in a cold storage wallet, deposit some ETH onto dYdX permissionless DEX, and short ETH perps in the same size as your ETH holdings - you are now delta neutral (but have basis risk and need to manage your margin) - this is a good alternative to being in stables and is endorsed by whales like GCR

GCR, Ezekiel X @GCRClassicimagine if instead of holding undercollateralized stablecoins [that are increasingly going to be hunted, seized, and possibly frozen by regulators] you could just hold BTC and if, risk averse, you could even short the BTC you hold, collect free funding, and be in synthetic fiatApril 4th 2022120 Retweets1,318 Likes

Autist notes on Gresham’s law: the above is a simplified explanation as space and time does not permit a deeper dive. Here are some sources for further study:

- Federal Reserve Bank of Minneapolis’ Quarterly Review, Winter 1986, page 17

- George Selgin’s essay for the Economic History Association and commentary for the Cato Institute

- Pecquet, G and Thies, C: “Money in occupied New Orleans, 1862–1868: A test of Selgin’s “salvaging” of Gresham’s Law”

- Frank Whitson Fetter’s “Some Neglected Aspects of Gresham's Law”

- Aiyagair’s “Gresham's Law in a Lemons Market for Assets”

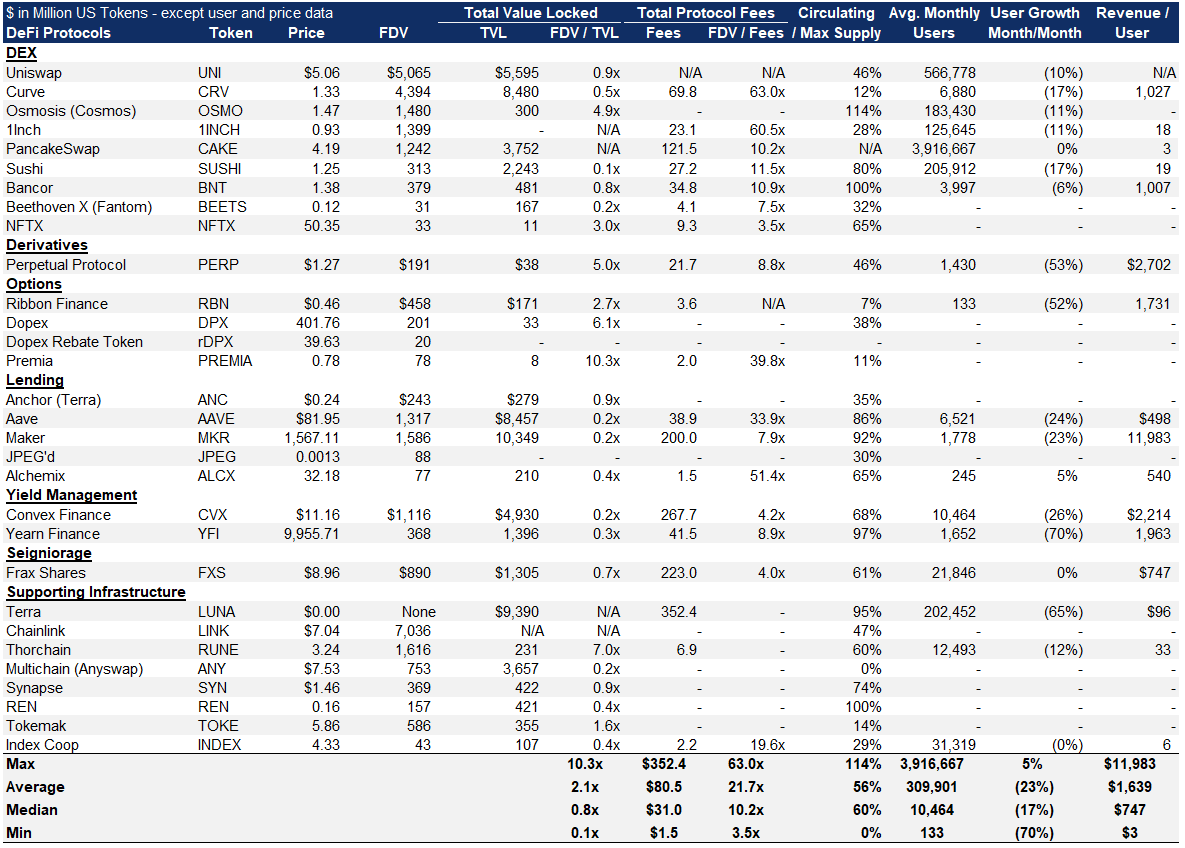

Comps

Multiples are down across the board - valuation update post planned soon!