Annual Chain Report: What Happened in 2022 and Where is the Industry Heading?

Data source: Footprint Analytics — Chain overview

This annual chain report looks at data from the past year on Footprint Analytics to identify critical trends among public chains.

In 2022, most headline crypto news did not involve chains per se. While the Three Arrows/BlockFi/Celcius/FTX collapses, Bitcoin legal tender adoption, the launch of crypto ETFs, etc., are all significant, this report looks at dynamics between the various L1 and L2 chains.

For retail and institutional investors: L1 and L2 chains have native tokens, so people look at the data to hypothesize about the potential growth of an ecosystem and, consequently, the appreciation in the price of those tokens.

Conversely, the collapse of an ecosystem means the death of its protocols. E.g., Anchor collapsed along with LUNA. Being overconfident in one chain or ecosystem can lead to losing one’s tokens or NFTs.

The optimal capital allocation in light of risk management is the million-dollar question. Our data and perspectives can help investors manage their risk.

Chain analysis also offers critical insights for developers. Developers must be highly aware of cross-chain trends, as deciding where to launch or expand a project is make-or-break. Influencing factors include ecosystem support, users and community, and performance. We touch on many of these factors when assessing DeFi, NFT, and GameFi sectors.

Finally, if you’re a researcher — at a VC, media outlet, or traditional financial institution — you have the incentive to be ahead of the curve. This report goes beyond the headlines and looks at the underlying data which moves the blockchain industry.

It will answer three questions:

- What is the most critical data from 2022, and how does it affect the outlook of the blockchain industry?

- What happened in the GameFi industry, and what could happen in the future?

- What happened in the NFT industry, and what could happen in the future?

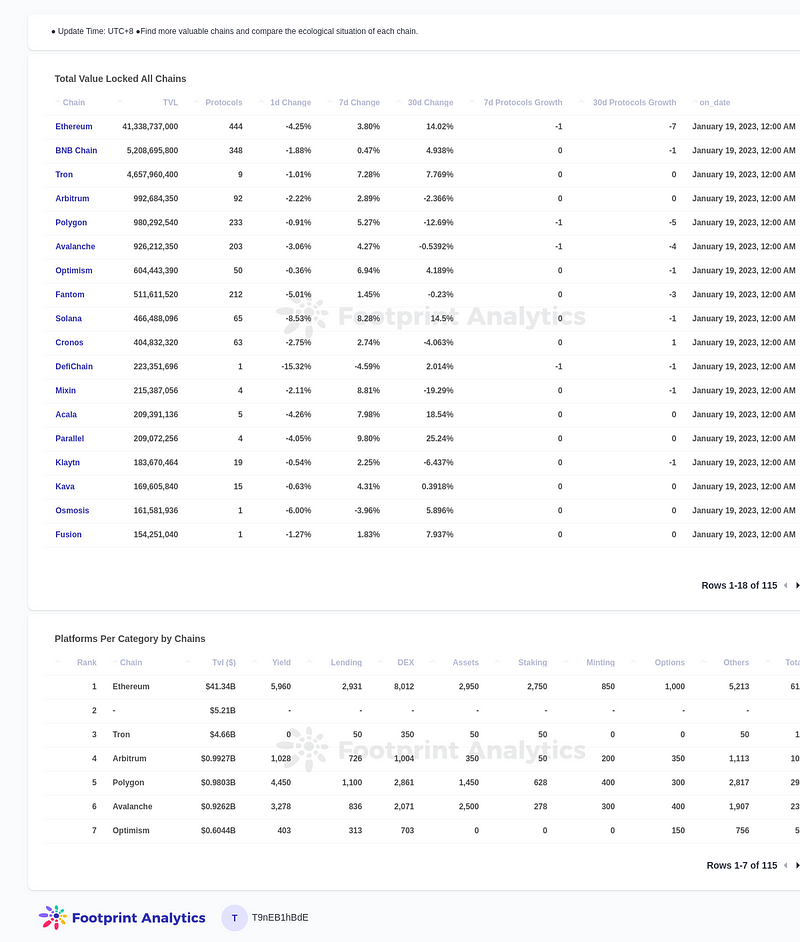

Overview of Chain Key Metrics

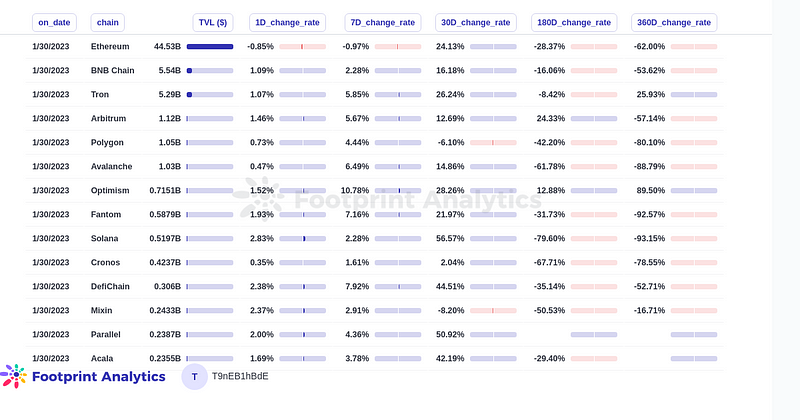

Top 5 Chains by TVL Key Metrics

Token market cap: N/A (Arbitrum does not have a native token)

Highlights from 2022 & Looking to 2023

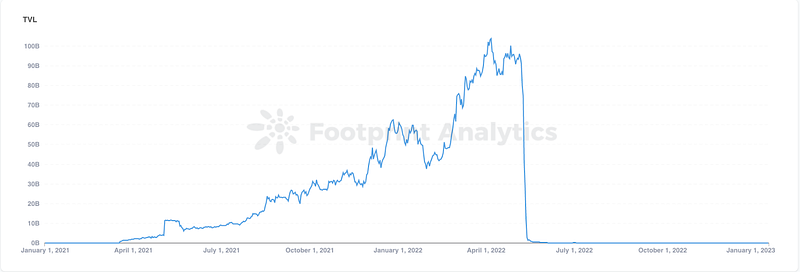

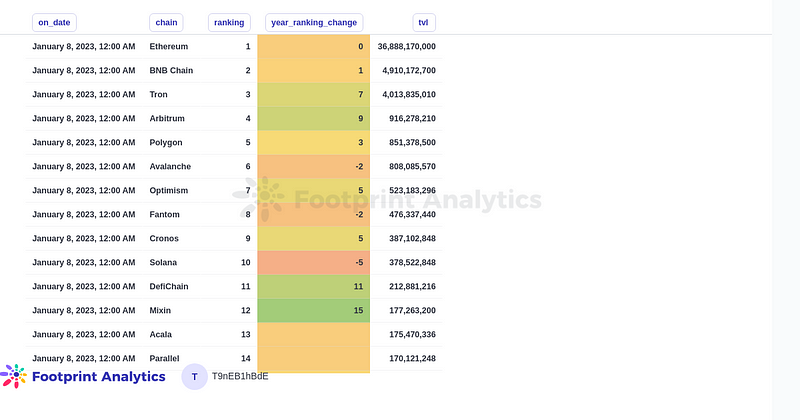

In 2022, several fastest-growing chains unexpectedly collapsed while others survived and thrived. If at the beginning of last year, you told crypto analysts that TRON would have 10x the TVL of Solana and Do Kwon was in hiding, they would think you were crazy — but that was the reality of this drama-filled year.

If anything, the year was characterized by unexpected fragility and reversals from some ecosystems, and equally surprising stability and resilience from others. Several former headliners like Terra, Cronos and Solana are no longer in the headlines for the right reasons, while Ethereum and Binance have become more relevant.

The impact on the future is that there will be significantly more skepticism toward DeFi projects. Between the beginning of May to the end, Terra Luna lost $96B of value.

Solana gained significant attention in 2020 and 2021 due to its fast transaction speeds and low transaction fees, which made it attractive for decentralized finance (DeFi) applications and other high-throughput use cases. However, from the heights of this extremely optimistic narrative, the Solana ecosystem has had a precarious slide, which included the collapse of its largest GameFi project, STEPN.

These are Arbitrum, Polygon, and Optimism. While there is one narrative that looks out for Ethereum-killers like Solana, Avalanche, etc., another is equally valid. I.e., Ethereum will be the primary base infrastructure of the blockchain, with the next bull run dominated by solutions built atop it.

While Ethereum is the most diversified when we look at the breakdown between GameFi, DeFi and NFT categories on the chain, BNB has several strengths. On the front end (facing the general public), it is buoyed by the world’s largest CEX, Binance, which has so far weathered the storm — which it caused, in part — after FTX collapsed. While most of its TVL is in DeFi, it is the 4th largest chain by market share of gamers (nearly 10%), attracts the most GameFi projects + developers, and is now getting into the NFT space. Being connected to the centralized entity is both a risk and an opportunity.

DeFi & Chains in 2022

2022 was a year both dominated by DeFi and one wherein DeFi eventually got relegated to relative obscurity by newer, trendier sectors of the blockchain industry.

While the Terra collapse made people realize the realistic limits of yield in crypto, DeFi remains the foundation of GameFi, where in-game assets can generate income while playing a game.

Interestingly, a large chunk of capital that fled from Terra stayed invested in DeFi rather than cashing out into other sectors or from crypto, as we reported here. It’s what caused Tron to become the 3rd largest chain. This shows that despite the risk, DeFi remains relevant.

As important as things that happened are things that didn’t. There was no Ethereum-killer, and in the area of DeFi, no other chain came close to taking Ethereum’s place as the network to hold, exchange, borrow, lend and stake one’s crypto assets.

This was caused by the flight of DeFi capital from Terra, as we found in this article by conducting on-chain data analysis.

Tron provides compatibility with Ethereum smart contracts through a pluggable smart contract protocol and is based on the improved consensus mechanism of dPoS (Delegated Proof of Stake), which ensures high TPS (transactions per second) throughout the network. Tron’s vision centered on reduced costs, accessible participation, and an easily scalable network. While reasonably innovative when it launched in 2018, there hasn’t been much ecosystem growth regarding the number of projects, with only 9 protocols on the chain.

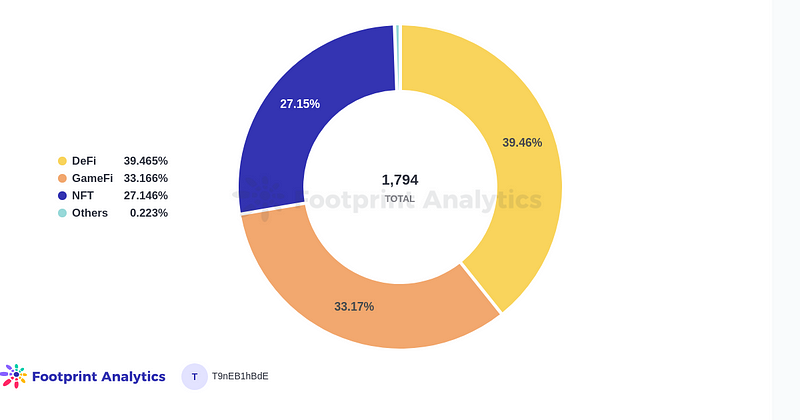

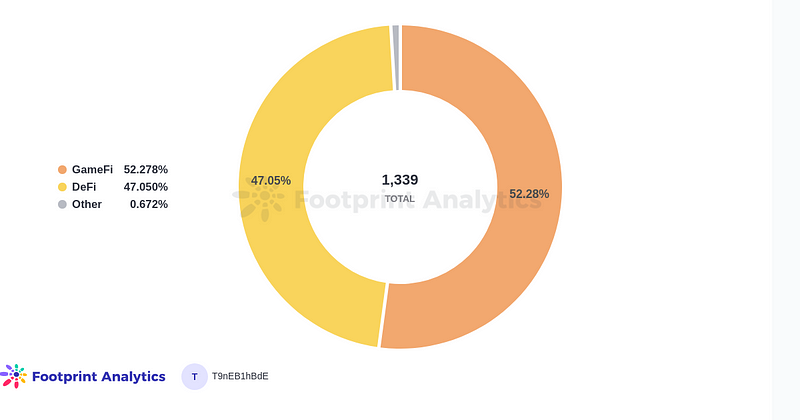

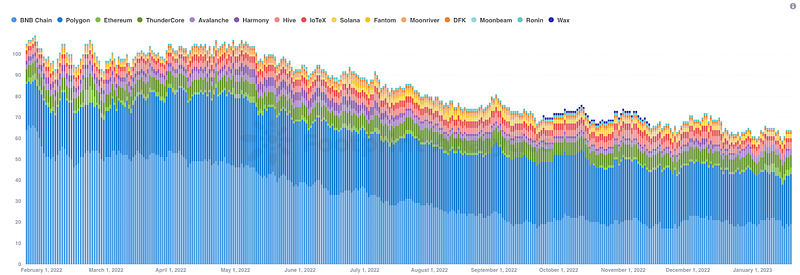

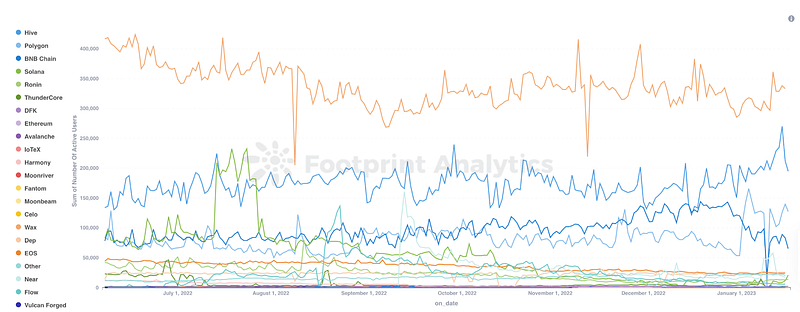

GameFi & Chains in 2022

Most newer games — especially those proving to have some staying power — are not being built on Ethereum. While Ethereum was originally the chain of choice for ambitious metaverse projects, i.e. Decentraland and The Sandbox, none of the top games by active users are on Ethereum.

Why big metaverse projects and not blockchain games? The new type of smaller blockchain games emerged in the last bull market after the congestion and network fee problems of Ethereum already became known, which are highly limiting for games that require frequent transactions. Hence other chains like BNB and L2s came into their own on the back of the GameFi boom.

Ethereum is tied for 4th for the number of active GameFi projects by chain. It remains to be seen whether upgrades to the Ethereum network in terms of fees and congestion will change this.

However, some of the most anticipated blockchain titles, such as Illuvium, will soon be released. Their performance will determine whether Ethereum can become a center for GameFi development.

In a roundabout way, Ethereum is making inroads via its L2s.

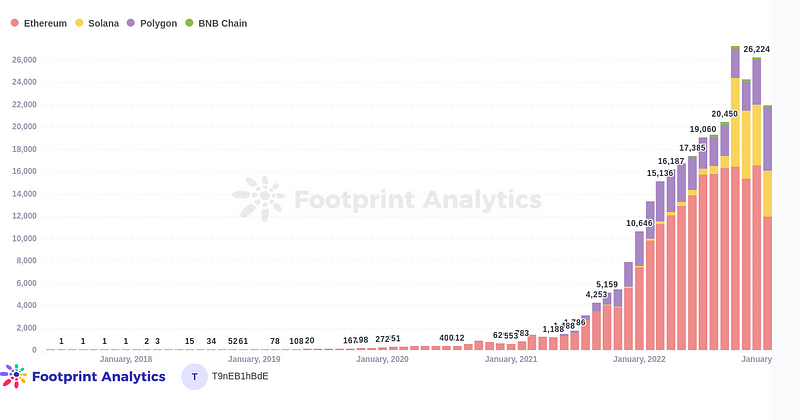

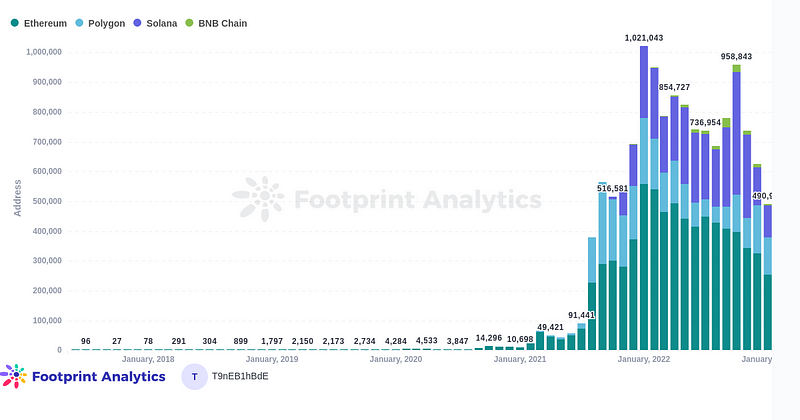

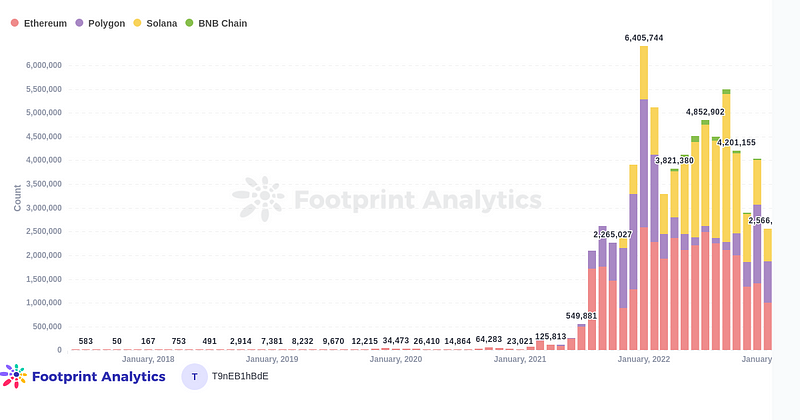

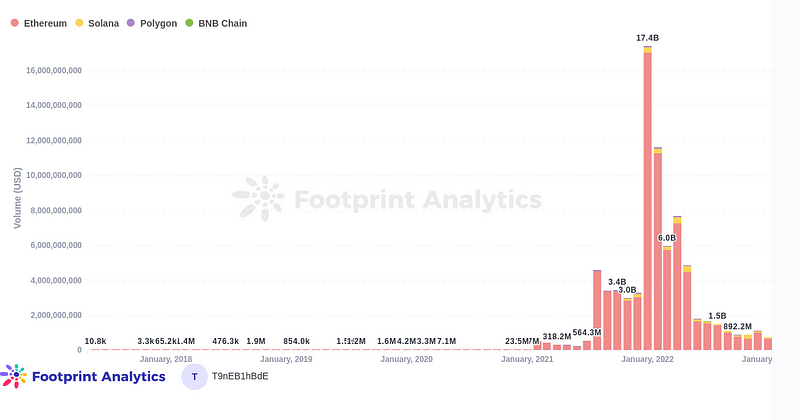

NFT & Chains in 2022

The initial explosion of NFT collections happened in 2021, and 2022 was the year when dozens of infrastructure projects emerged to make the market more efficient and accessible.

Seeing the limitations of OpenSea, developers began experimenting with different fee and tokenomic models, creating LooksRare and X2Y2. Combining all these, aggregators like Rarible emerged. There is also experimentation with AMM models, e.g., SudoSwap, and exclusive, invite-only marketplaces like Foundation.

With the novelty of PFP collections having worn off, 2022 saw a massive explosion of creative energy in NFT tech and product development. While most of the trading volume remained on Ethereum, other ecosystems, namely Polygon and Solana, began attracting communities and developers.

- Ethereum dominates the NFT sector, and the secondary ecosystems to watch are Polygon, Solana, and BNB Chain.

Solana has many projects built on it, yet all the money is still on Ethereum. This can indicate that it is an ecosystem waiting to blow up (in a good way) once macroeconomic conditions turn positive.

Bonus: New Chains in 2022 and 2023

Does the world need more L1s? Many of the former Diem team from Facebook would think so. Aptos is the most notable new L1 to launch in 2022, and comes with several breakthroughs. For example, it could be more efficient and secure than other chains thanks to its Byzantine fault tolerant engine, parallel transaction execution, and purpose-built programming language.

Another L1 built on the Diem technology and the Move programming language is Sui, which is expected to launch in 2023.

However, suppose 2022 has taught us anything, it’s this: Even in the most optimistic, hyperinflationary conditions in history, it is extremely hard for strong competitors — think Solana and Avalanche — to approach incumbents in the crypto industry.

While Aptos is undoubtedly built on incredibly strong technology on the back of $350M in funding, the continued market share of Ethereum and its L2s shows that, even in the crypto industry, developers are risk averse when it comes to throwing their chips in with an entirely new ecosystem, never mind language.

This piece is contributed by Footprint Analytics community.

The Footprint Community is a place where data and crypto enthusiasts worldwide help each other understand and gain insights about Web3, the metaverse, DeFi, GameFi, or any other area of the fledgling world of blockchain. Here you’ll find active, diverse voices supporting each other and driving the community forward.

Footprint Website: https://www.footprint.network

Discord: https://discord.gg/3HYaR6USM7

Twitter: https://twitter.com/Footprint_Data