Islamic Finance FAQ

We have repeatedly addressed the topic of Islamic finance in the cryptocurrency business. But understanding this issue is impossible without understanding on the basis of which principles Islamic finance itself functions. In this article we will answer the most important questions related to the work of the Islamic financial system and Islamic banks.

Halal or Haram? If you want to share your opinion about cryptocurrencies and blockchain technologies, please welcome Telegram chat. We need to know what you think!

The word "Riba" means excess, increase or addition, which correctly interpreted according to Shariah terminology, implies any excess compensation without due consideration (consideration does not include time value of money). This definition of Riba is derived from the Quran and is unanimously accepted by all Islamic scholars.

The meaning of Riba has been clarified in the following verses of Quran (Surah Al Baqarah 2:278-9)

"O those who believe; fear Allah and give up what still remains of the Riba if you are believers. But if you do not do so, then be warned of war from Allah and His Messenger. If you repent even now, you have the right of the return of your principal; neither will you do wrong nor will you be wronged."

2. What is interest and what is the difference between interest and Riba?

The origination of term interest dates back to 17th century with the emergence of banking system at global level. Interest means giving and/or taking of any excess amount in exchange of a loan or on debt. Hence, it carries the same meaning/value as that of Riba as defined in the previous question. Further, it is narrated that “the loan that draws interest is Riba”.

3. What are the revelations/verses in Holy Quran regarding prohibition of Riba/interest?

There are four sets of revelations about Riba which were revealed on different occasions.

First Revelation: In Surah-Ar-Rum, verse 39 , dealing in Riba has been discouraged in the following words:

"And whatever riba you give so that it may increase in the wealth of the people, it does not increase with Allah." [Surah Ar-Rum 30:39]

Second Revelation: Muslims have been informed about the practice of taking riba by Jews in Surah An-Nisaa:

"And because of their charging riba while they were prohibited from it." [Surah An-Nisaa 4-161]

Third Revelation: Riba/Interest has been abolished in the third verse of Surah Ali-'Imran. The prohibition of riba is laid down in the following words:

"O those who believe do not eat up riba doubled and redoubled." [Surah Al-e-Imran 3- 130]

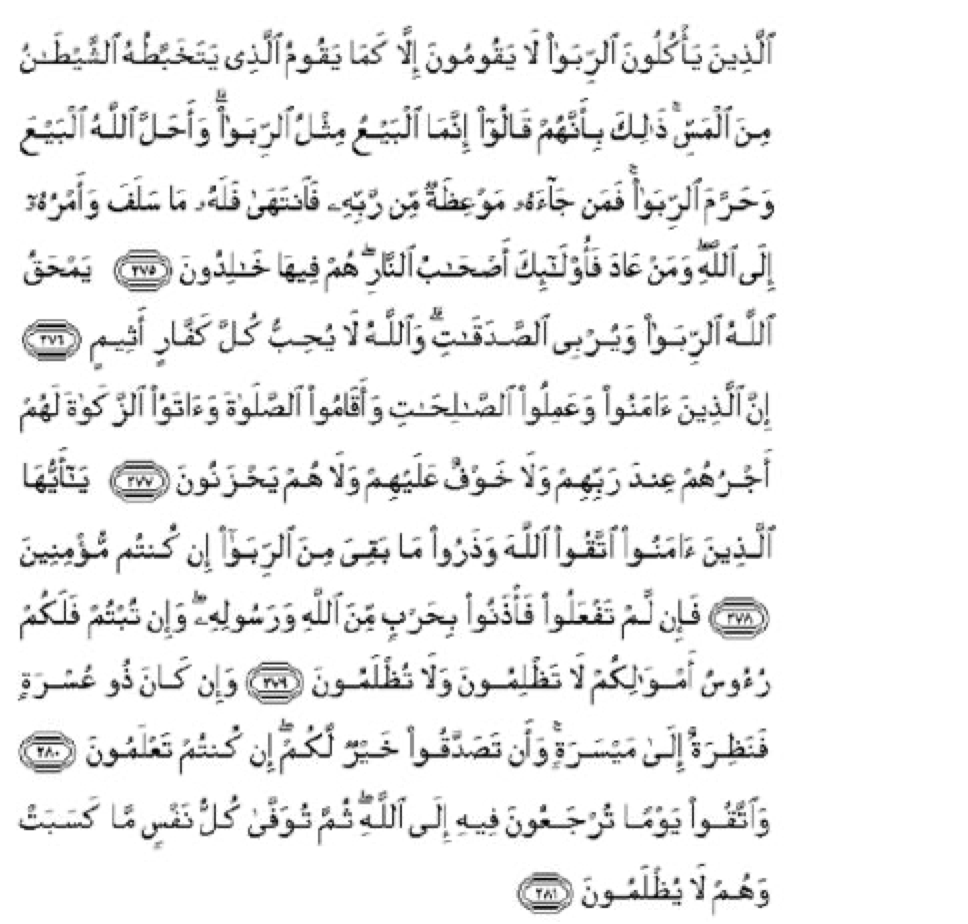

Fourth Revelation: In the fourth revelation, Riba has categorically been prohibited in all its forms. The following set of verses is found in the Surah Al-Baqarah, verse 275-281 in the following words:

"Those who take interest will not stand but as stands whom the demon has driven crazy by his touch. That is because they have said: 'Trading is but like riba'. And Allah has permitted trading and prohibited riba. So, whoever receives an advice from his Lord and stops, he is allowed what has passed, and his matter is up to Allah. And the ones who revert back, those are the people of Fire. There they remain for ever. Allah destroys riba and nourishes charities. And Allah does not like any sinful disbeliever. Surely those who believe and do good deeds, establish Salah and pay Zakah, have 11 their reward with their Lord, and there is no fear for them, nor shall they grieve. O those who believe, fear Allah and give up what still remains of the riba if you are believers. But if you do not, then listen to the declaration of war from Allah and His Messenger. And if you repent, yours is your principal. Neither you wrong, nor be wronged. And if there be one in misery, then deferment till ease. And that you leave it as alms is far better for you, if you really know. And be fearful of a day when you shall be returned to Allah, then everybody shall be paid, in full, what he has earned. And they shall not be wronged." [Surah Al-Baqarah 2:275-281]

4. Does the prohibition of Riba apply equally to the loans obtained from or extended to Muslims as well as non-Muslims?

With respect to the receipt and payment of interest, there is no distinction between Muslims and non-Muslims or between individuals and states because interest is prohibited not only in Islamic scriptures but also in other religious scriptures of the world as given in questions above. Therefore, prohibitions of interest apply to Muslims as well as to non-Muslims.

5. What are the basic principles of Islamic banking?

- There are at least six basic principles which are taken into consideration while executing any Islamic banking transaction. These principles differentiate a financial transaction from a Riba/interest-based transaction to an Islamic banking transaction.

- Sanctity of contract: Before executing any Islamic banking transaction, the counter parties have to satisfy whether the transaction is halal (valid) in the eyes of Islamic Shariah. This means that Islamic bank’s transaction must not be invalid or voidable. An invalid contract is a contract, which by virtue of its nature is invalid according to Shariah rulings. Whereas a voidable contract is a contract, which by nature is valid, but some invalid components are inserted in the valid contract. Unless these invalid components are eliminated from the valid contract, the contract will remain voidable.

- Risk sharing: Islamic jurists have drawn two principles from the saying of prophet Muhammad (SAW). These are “Alkhiraj Biddamaan21” and “Alghunun Bilghurum22”. Both the principles have similar meanings that no profit can be earned from an asset or a capital unless ownership risks have been taken by the earner of that profit. Thus in every Islamic banking transaction, the Islamic financial institution and/or its deposit holder take(s) the risk of ownership of the tangible asset, real services or capital before earning any profit there from.

- No Riba/interest: Islamic banks cannot involve in riba/interest related transactions. They cannot lend money to earn additional amount on it. However as stated in point No. 2 above, it earns profit by taking risk of tangible assets, real services or capital and passes on this profit/loss to its deposit holders who also take the risk of their capital.

- Economic purpose/activity: Every Islamic banking transaction has certain economic purpose/activity. Further, Islamic banking transactions are backed by tangible asset or real service.

- Fairness: Islamic banking inculcates fairness through its operations. Transactions based on dubious terms and conditions cannot become part of Islamic banking. All the terms and conditions embedded in the transactions are properly disclosed in the contract/agreement.

- No invalid subject matter: While executing an Islamic banking transaction, it is ensured that no invalid subject matter or activity is financed by the Islamic financial transaction. Some subject matter or activities may be allowed by the law of the land but if the same are not allowed by Shariah, these cannot be financed by an Islamic bank.

6. What is meant by Shariah/Islamic Law?

Shariah lexically means a way or path. In Islam Shariah refers to the divine guidance and laws given by the Holy Quran, the Hadith (sayings) of the Prophet Muhammad (Peace Be Upon Him) and supplemented by the juristic interpretations by Islamic scholars. Shariah embodies all aspects of the Islamic faith, including beliefs and practices. Islamic Shariah or the divine law of Islam is derived from the following four sources:

2. The Sunnah of the Holy Prophet (Peace Be Upon Him)

3. Ijma’ (consensus of the Ummah)

7. The end result of Islamic Banking and Conventional Banking is the same. Why do they appear similar?

The validity of a transaction does not depend on the end result but rather the process and activities executed and the sequence thereof in reaching the end. If a transaction is done according to the rules of Islamic Shariah it is halal even if the end result of the product may look similar to conventional banking product.

Similarly, if a person is feeling hungry, he may steal a piece of bread and eat or alternatively buy a piece of bread to eat. The apparent end result would be same but one is permissible in Shariah and the other is not allowed.

The same is also true for Islamic and conventional banking. Therefore, it can be concluded that it is the underlying transaction that makes something “Halal” (allowed) or “Haram” (prohibited) and not the result itself. Apparently, Islamic banks may look similar to conventional banks, however the contracts and product structures used by Islamic banks are quite different from that of the conventional bank. In the verse 2:275 of the Holy Quran, Allah the Almighty has responded to the apparent similarity between trade and interest by resolutely informing that he has permitted trade and prohibited Riba (though they may look similar to someone).

8. If Islamic banks do not invest in interest based activities then how do they generate profit to pay to their customers?

The Islamic bank uses its funds in various trade, investment and service related Shariah compliant activities and earns profit thereupon. The profit earned from such activities is passed on to the depositors according to the agreed terms.

9. Are not Islamic banks just paying interest and dressing it as profit on trade and investments?

No, Islamic banks accept the deposits either on profit and loss sharing basis or on qard basis. These deposits are deployed in financing, trading or investment activities by using the Shariah compliant modes of finance. The profit so earned by the bank is passed on to the depositors according to the pre-agreed ratio which, therefore, cannot be termed as interest.

10. Are Islamic banks work only for Muslims?

The teachings of Islam are not confined to Muslims, rather these equally address the non-Muslims due to their universal nature. The basis of Islamic banks is laid down on ethical values and socially responsible system. The values like justice, mutual help, free consent and honesty on the part of the parties to a contract, avoiding fraud, misrepresentation and misstatement of facts and negation of injustice or exploitation form the basic principles of Islamic banking. Therefore, the principles of Islamic banking lead the economic system to achieve the common good and economic prosperity. On this premise, Islamic banking becomes a viable option for everyone irrespective of their religion.

Halal or Haram? If you want to share your opinion about cryptocurrencies and blockchain technologies, please welcome Telegram chat. We need to know what you think!