Analyzing the potential impact DeFi has on ether supply and demand

Decentralized financial (DeFi) applications have risen rapidly in the broader digital currency ecosystem, presenting one of the leading use cases for the Ethereum network. Over the past year, several high profile DeFi platforms have launched to considerable market interest. While each DeFi platform has unique characteristics, and in many cases differing services and business models, one common thread amongst the majority of them, is the use of ether (Ethereum’s native token) as collateral on the platform.

As the demand for decentralized financial services grows, so does the demand for ether on these platforms. Given the rising demand for ether across these new DeFi platforms, we seek to quantify the demand and supply dynamics of ether over the next few years. Principally, we seek to determine the possible effect DeFi can have on the price of ether in a conservative projected scenario.

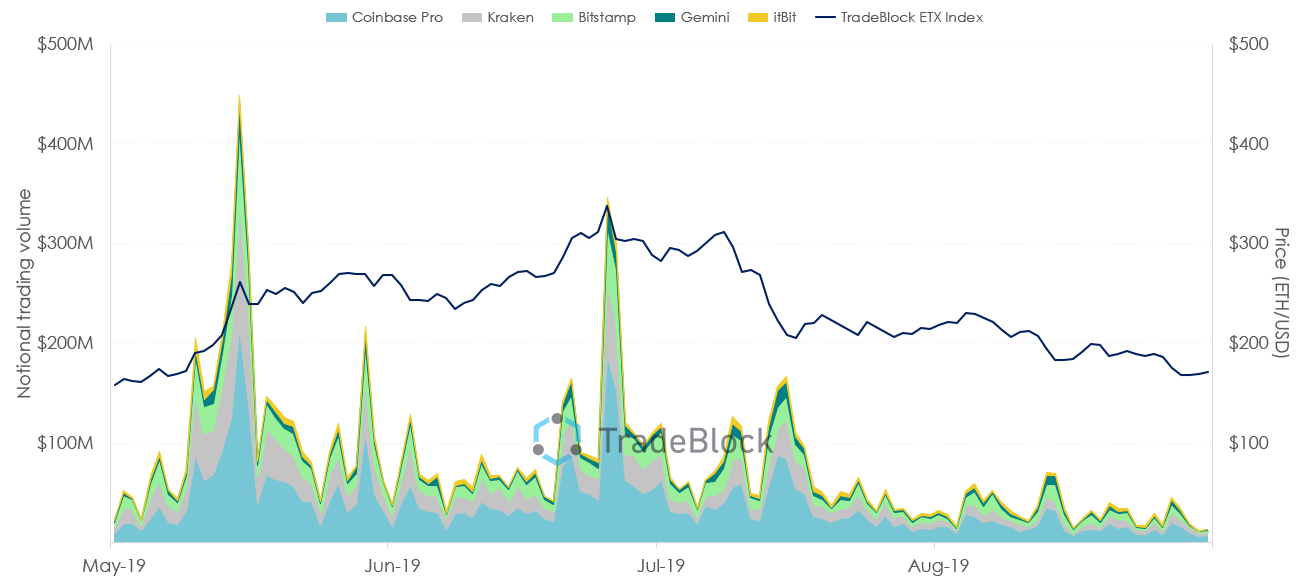

Over the past several months, after the space reached a local bottom in 2018, ether prices have experienced an uptick as capital has broadly flowed into the digital currency space. In recent weeks, amid turbulent markets, some of these gains were returned as alt-coins have slumped. In the figure below we diagram ether prices and trading volume across the largest US accessible spot exchanges over time.

Figure 1: Ether prices and notional trading volume over time

Background on decentralized financial services

DeFi platforms offer similar financial services as traditional centralized companies, however they exist in a trustless ecosystem for which the dependency on intermediaries is greatly reduced. DeFi platforms incorporate smart contract functionality into transactions that often require collateral deposits in the form of a digital asset to ensure proper engagement between communicating parties.

Similar to traditional financial companies, DeFi platforms offer collateralized debt products (e.g. loans/ bonds/ derivatives/ mortgages); however, these products are collateralized with digital currencies instead of other assets. Because decentralized platforms do not rely on third party intermediaries to ensure trust between communicating parties, these platforms often rely on collateral deposited in smart contracts to ensure timely and appropriate payment per terms structured in the contract. While many decentralized platforms offer various collateral types, the majority of collateral locked in these contracts is in the form of ether.

Demand for ETH on decentralized financial applications grows

Since the inception of DeFi platforms, the amount of ETH added as collateral across these applications has increased significantly. In the figure below we diagram the amount of ETH collateralized across DeFI platforms in the last year. As shown, the amount of ETH collateralized across DeFi platforms has decreased recently after hitting an all-time high earlier this year.

Figure 2: Total ETH collateralized across DeFI platforms over time

Data for chart sourced from DeFi Pulse

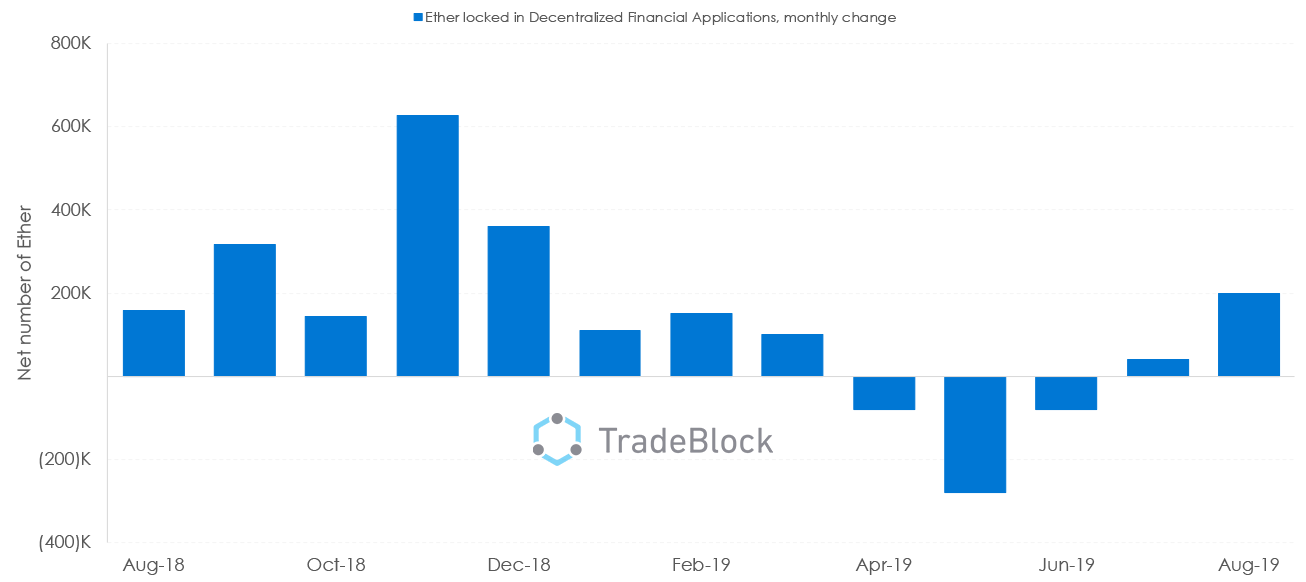

Year-over-year, the average monthly growth rate in net new ETH added across DeFi platforms stood at ~17%. In the figure below we diagram the amount of net ether (ETH added subtracted by ETH removed) flowing into DeFi platforms each month.

Figure 3: Net ETH collateralized on DeFi platforms by month

Data for chart sourced from DeFi Pulse

Over the last year, more than 125,000 ETH, on average, were added across DeFi platforms each month. Analogously, the average daily demand for ETH each day, over this one year period, stood at just over 4,000. Over the last full month period (July 2019), the average daily demand declined to approximately 1,300 ETH per day.

Estimating future daily ETH demand

In order to estimate demand in the future, we must make some assumptions. We take a conservative approach analyzing one possible scenario that assumes as platforms and markets mature, their growth rate subsides.

With this assumption in place, we arrive at a modest – compared to the average rate of 17% in the last year – projected average monthly growth rate of 5%. Given the accelerated growth in new ETH added as collateral in these platforms over the past year, and the recent slow down, it is not unreasonable to assume the growth rate slows as platform market penetration nears saturation points.

Additionally, as multi-collateral contracts arise, it is expected that other digital assets will be used as collateral in DeFi platforms. The use of alternate digital currencies, as collateral, could reduce the demand for ETH.

In estimating future demand, we first start our projections from the current average daily demand level of 1,300 ETH (the daily demand for July 2019). We assume a projected average monthly growth rate of 5% per month moving forward. At a constant 5% monthly growth rate for the next year (ending December 2020) we arrive at a demand of ~3,000 ETH per day.

Estimating future daily ETH supply

The current yearly new issuance rate for ether is ~4.65%. The new issuance supply rate was reduced earlier this year when mining block reward issuance was reduced from 3 ETH to 2 ETH, during the Ethereum network’s Constantinople upgrade. In the figure below, we diagram the ETH supply rate over time until the present.

The network is expected to undergo another upgrade, Serenity, in early 2020, which could see new ETH issuance fall considerably. Upon successful implementation of Serenity, Ethereum developers expect the new issuance rate to decline to between 0.25%-2%. Ethereum’s new issuance supply schedule is not fixed, and, upon transition to proof-of-stake, it is uncertain what the exact new issuance supply rate will be. In our scenario, we will assume a new issuance rate beginning in Feb 1, 2020 will be reduced to a conservative estimate of 1%. It is important to note, however, that roadmap delays may result in a considerable shift in the estimated supply rate reduction.

Additionally, the amount of ETH demanded for DeFi is dependent on the USD equivalent value and not on the value of ether. In other words, if the price of ether rises/declines the USD equivalent demand for loans and decentralized financial services would not necessarily increase/decrease over time, while the ether demand would in order to maintain approximately the same USD equivalent demand as before the ether price change.

This appears to have played out recently, when the amount of ETH collateralized in the Maker platform declined as the price of ether accelerated earlier this year

Daily defi ETH demand could outstrip new daily supply by 2020

Assuming a 1% yearly supply rate beginning in February 2020, the daily new ETH supply rate by November 2020 would be ~3,000. Taking into consideration our daily ETH demand projections outlined in the section above, we arrive at a projection at which point daily ETH demanded for collateral in DeFi services would equal the daily new supply rate.

That is to say, if demand grows further or if the new supply rate is reduced by a greater percentage, daily demand for ETH in DeFi services would consistently outstrip the new supply of ETH by November 2020. While daily ETH demand has outstripped new supply over brief periods of time in the past, this has not consistently occurred as supply has typically been considerably greater than the demand.

It is also important to note, however, that if the price of ether rises exorbitantly due to speculation or other, this would reduce the amount of ETH needed for lockup across DeFi platforms. As such, the daily demand (denominated in ether) for use in DeFi would decline if the price of ether rose dramatically while the demand for DeFi services rose at a slower pace than the price.

In fact, on large intra-day price rises, the daily demand for ETH for lockup across DeFi platforms typically declines, and on days the price declines, the demand rises as shown in the figure below. This is because on sharp declines in price, ETH collateral needed across DeFi platforms increases, whereas when price rises, the amount of collateral needed declines, and market participants can remove some of their ETH held as collateral.

Concluding remarks

It is our hope that this report can shed light on how decentralized financial services may have a tangible impact on ether demand. Our conservative projections demonstrate that in November 2020, the demand for ether, just from DeFi services, could outstrip new supply. There are also various other decentralized applications (dApps) that could result in further demand for ether such as games, medical dapps, and others. On the contrary, it is also important to note that if ether supply is not reduced as considerably as expected in the future, this could result in excess ether that significantly outstrips demand from DeFi and/or other dApps.