Tax brackets married filing jointly

The IRS modifies more than 40 tax provisions for inflation on a yearly basis. This is done to avoid “bracket creep,” which occurs when taxpayers are forced into higher tax rates or have the value of their credits and deductions decreased owing to inflation rather than an increase in real income. Looking for tax brackets married filing jointly?

Prior to 2018, the IRS utilised the Consumer Price Index (CPI) to calculate inflation.

The IRS now uses the Chained Consumer Price Index (C-CPI) to alter income thresholds, deduction levels, and credit values in accordance with the Tax Cuts and Jobs Act of 2017

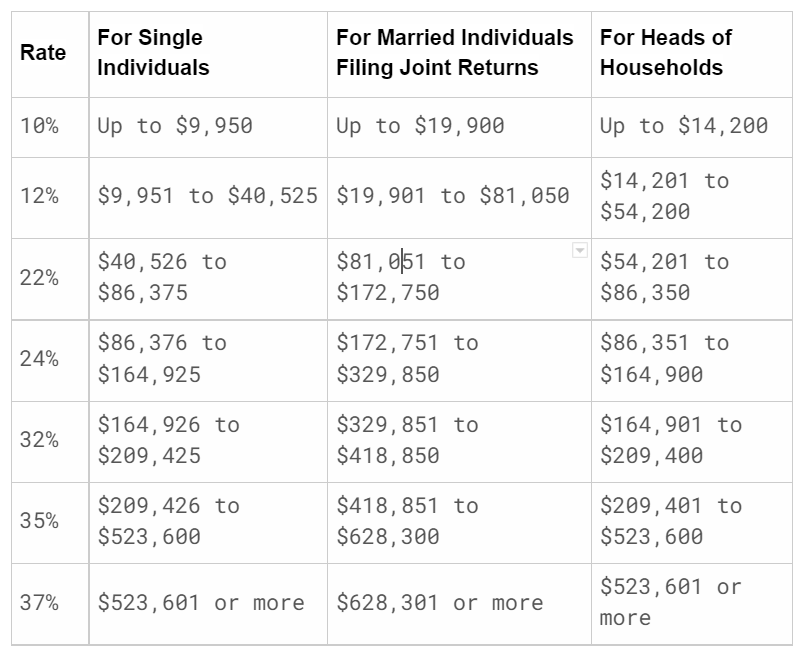

Federal Income Tax Rates and Brackets for 2021

The following income ceilings will be adjusted for inflation in 2021 for all tax categories and filters: (Tables 1). Taxpayers having taxable income of $523,600 or more for single filers and $628,300 or more for tax brackets married filing jointly will be whacked by the top marginal income tax rate of 37 percent.

2021 Federal Income Tax Brackets and Rates for Single Filers, Married Filing Jointly, and Heads of Households

2021 Federal Income Tax Brackets and Rates for Single Filers, Married Filing Jointly, and Heads of Households

Personal Exemption and Standard Deduction in 2021The standard deduction will increase by $150 for solo filers and $300 for tax brackets married filing jointly.

The personal exemption will be repealed in 2021.Alternative Minimum Tax (AMT) in 2021

In the 1960s, the Alternative Minimum Tax (AMT) was enacted to discourage high-income people from evading the individual income tax. High-income people must calculate their tax bill twice under this parallel tax income scheme: once under the regular income tax system and again under the AMT. The taxpayer must then pay the higher of the two amounts.

The Alternative Minimum Taxable Income (AMT) adopts a different definition of taxable income (AMTI). To keep low- and middle-income taxpayers out of the AMT, they can exclude a considerable portion of their income. This exemption, however, is phased away for high-income individuals. The AMT is charged at two different rates: 26% and 28%.

For 2021, the AMT exemption level for singles is $73,600, and for tax brackets married filing jointly, it is $114,600.

Excess AMTI of $199,900 for all taxpayers ($99,950 for tax brackets married filing jointly separate returns) will be subject to the AMT rate of 28% in 2021.

Once a taxpayer's AMTI reaches a particular level, AMT exemptions are phased down at 25 cents every dollar earned. The exemption will begin to phase out in 2021 at $523,600 in AMTI for solo filers and $1,047,200 for tax brackets married filing jointly.

Earned Income Tax Credit in 2021

If the filer has no children, the maximum Earned Income Tax Credit in 2021 is $543 for single and joint filers . For one child, the maximum credit is $3,618; for two children, it's $5,980; and for three or more children, it's $6,728. All of them are minor increases compared to 2020.

The child tax credit is worth $2,000 per qualified child and is not inflation-adjusted. The refundable element of the Child Tax Credit, on the other hand, is inflation-adjusted but will continue at $1,400 in 2021.

Deduction for Qualified Business Income in 2021 (Sec. 199A)

The Tax Cuts and Jobs Act allows pass-through enterprises to deduct 20% of eligible company income up to $164,900 for single taxpayers and $329,800 for married taxpayers.

The first $15,000 in gifts to any person will be tax-free in 2021. The exclusion for gifts to spouses who are not US citizens has been raised to $159,000.