Business - Tesla and the markets

Elon Musk’s latest madcap scheme: taking Tesla private

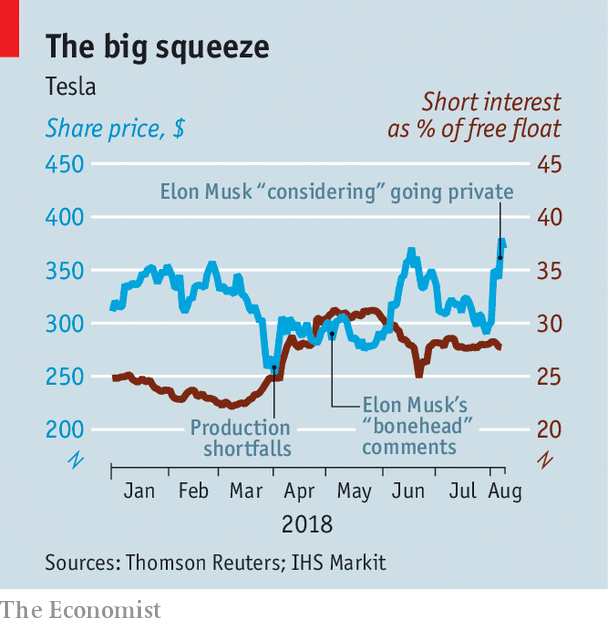

“I WISH we could be private with Tesla.” So said an exasperated and exhausted Elon Musk to Rolling Stone last November. Tesla’s rise has been remarkable. In 15 years it has taken on established carmakers to become the world’s leading manufacturer of electric cars. But the journey has been bumpy. Of late Mr Musk says his company has been in “production hell” trying to increase output of the Model 3, a whizzy mass-market saloon. While on its quest to change the world, Tesla has frequently missed its production targets and has never made an annual profit. Feeling the heat, Mr Musk earlier this year lashed out at share analysts for “bonehead” questions, and has derided the army of short sellers targeting it.

Yet it still came as a shock when, on August 7th, Mr Musk revealed his intention to take Tesla private in an extraordinary tweet. He claimed that he had lined up enough money to buy out the firm at $420 per share, roughly a fifth above the share price at the time. The chaos surrounding the tweet led to a brief suspension of trading of its shares on the NASDAQ stock exchange. Then Tesla released a memo confirming Mr Musk’s plan. He added details in subsequent tweets suggesting this was more than a lark. By the end of the day the firm’s shares were up sharply, dealing a costly blow to the shorts (see chart).

Mr Musk’s wish to depart from the public market is understandable, though of late he seems to have made some peace with its constraints. At a quarterly-earnings call on August 1st he said output of the Model 3 was rising and forecast profits soon. He even apologised to analysts. But private backers with deep pockets would let him expand at his own pace.

Can he achieve the unlikely yet again? One potential snag might be his cavalier use of tweets to drop his latest bombshell. American regulators have ruled that firms are permitted to disclose financial information using social media, but they must not mislead investors. They will be watching to see if his claim of having “funding secured” is borne out.

Another concern is the sheer size of the proposed deal. The largest buyout to date, the takeover by Kohlberg Kravis Roberts of RJR Nabisco in 1989, was worth $64bn in today’s money. Yet Mr Musk may not need the $70bn-80bn (including nearly $10bn of debt) at which Tesla would be valued at $420 per share. Some reckon he would require less than $40bn in financing if his own stake (about a fifth of the firm) and those of other big public investors were rolled into the new entity.

Mr Musk has given no details of where the cash will come from, but the source might well be foreign. Tencent, a Chinese internet giant, already holds a big stake in Tesla. Japan’s SoftBank, which has thrown vast sums at technology firms through its Vision Fund, might be keen. But the most likely investor is Saudi Arabia. Reports surfaced this week that the oil kingdom’s sovereign-wealth fund had bought shares in Tesla worth around $2bn.

Even if Mr Musk can rally the moneymen, going private may not prove a smooth ride. There may be political opposition to large foreign investments in an American car firm. Many punters who have held onto Tesla shares through the dark days made clear on Twitter that they did not want to sell. Mr Musk promised this week to create a special investment vehicle that would allow them and employees to “remain shareholders”, but experts say such an unorthodox and complex arrangement may hit legal snags. Then even Tesla’s accommodating board (which has already discussed this proposal) might be forced to reject it. Public or private, Tesla will keep Mr Musk running at full tilt.