Stocks Steady as China Sours Mood; Dollar Dips: Markets Wrap

- Beijing Covid cases, China tech stocks a drag; US futures rise

- Treasuries pare Friday advance as Fed rate path weighed

Asian stocks traded mixed Monday as investors assess the impact of China’s Covid policies on growth and the outlook for the world’s largest economies. The dollar and Treasuries retreated.

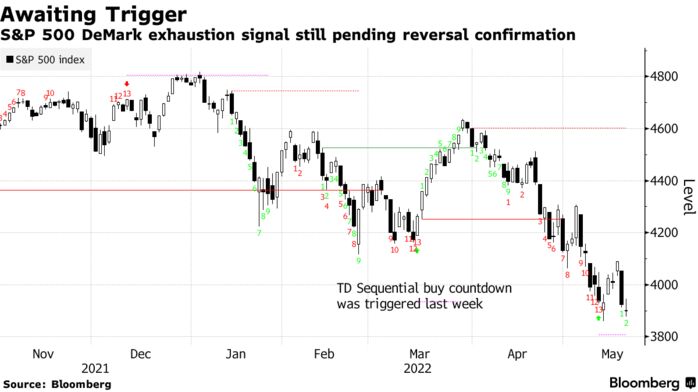

Equities rose modestly in Japan, but a slide in Chinese tech stocks and a virus outbreak in Beijing weighed on an MSCI Inc. gauge of the region’s stocks. Nasdaq 100 and S&P 500 futures jumped about 1% after the S&P 500 dropped for a seventh straight week in a stretch of weakness not seen since 2001.

Beijing reported a record number of Covid cases, reviving concerns about a lockdown. China’s stringent adherence to Covid Zero has stifled economic growth and prompted banks last week to cut a key interest rate for long-term loans by a record amount. Still, the one-year loan prime rate — the de facto benchmark lending rate — was kept unchanged.

“It seems that while there is an initial attempt to ride on some dip-buying sentiments from Wall Street, an increase in virus cases in Beijing is putting a cap on risk sentiments in the region, with China’s zero-Covid policy set to remain for the foreseeable future,” said Jun Rong Yeap, a market strategist at IG Asia.

A dollar gauge declined. The Australian dollar gained after a weekend election delivered a clear outcome, with Labor ousting the Liberal-National coalition. Treasuries pared Friday’s advance as traders debate the Federal Reserve’s tightening path amid mounting worries about an economic slowdown. Bitcoin recovered from some weekend weakness to trade around $30,000.

Investors are grappling with concerns about an economic slowdown and prospects for more monetary tightening. The war in Ukraine is fanning commodity prices, and supply chains remain disrupted by China’s adherence to its Covid zero policy.

“As macro-economic concerns stemming from aggressive monetary tightening, the Russia-Ukraine conflict and China’s stringent Covid lockdowns persist, we anticipate great volatility in the market,” Louise Dudley, portfolio manager global equities at Federated Hermes Ltd., said in a note.

Minutes of the most recent Fed rate-setting meeting will give markets insight this week into the US central bank’s tightening path. St. Louis Fed President James Bullard said the central bank should front-load an aggressive series of rate hikes to push rates to 3.5% at year’s end, which if successful would push down inflation and could lead to easing in 2023 or 2024.

Here are some key events to watch this week:

- Atlanta Fed President Raphael Bostic, Kansas City Fed President Esther George speak at events Monday

- ECB Governing Council members Robert Holzmann and Joachim Nagel, BOE Governor Andrew Bailey discuss inflation at event Monday

- Eurozone S&P Global PMIs Tuesday

- US new home sales, S&P Global PMIs Tuesday

- Reserve Bank of New Zealand rate decision Wednesday

- FOMC minutes Wednesday

- ECB publishes its Financial Stability Review Wednesday

- Bank of Korea rate decision Thursday

- US GDP, initial jobless claims Thursday

- US core PCE price index; personal income and spending; wholesale inventories; University of Michigan consumer sentiment Friday